The short answer is yes, it can happen, but the path is narrower and slower than the scare version makes it sound. And for a real HOA, as opposed to a condo association, whether your board can foreclose at all comes down to one document: your declaration. Not the state statute. Your own governing papers.

First, figure out which kind of association you're in

This is the fork everything hangs on. Condominiums fall under the Condominium Property Act. Most other communities, meaning planned developments, townhome rows, and single-family neighborhoods, fall under the Common Interest Community Association Act, or CICAA. Check your recorded declaration: a declaration of condominium means you're a condo, while covenants for a planned community mean you're an HOA. The two are not governed the same way, and that difference is the whole ballgame.

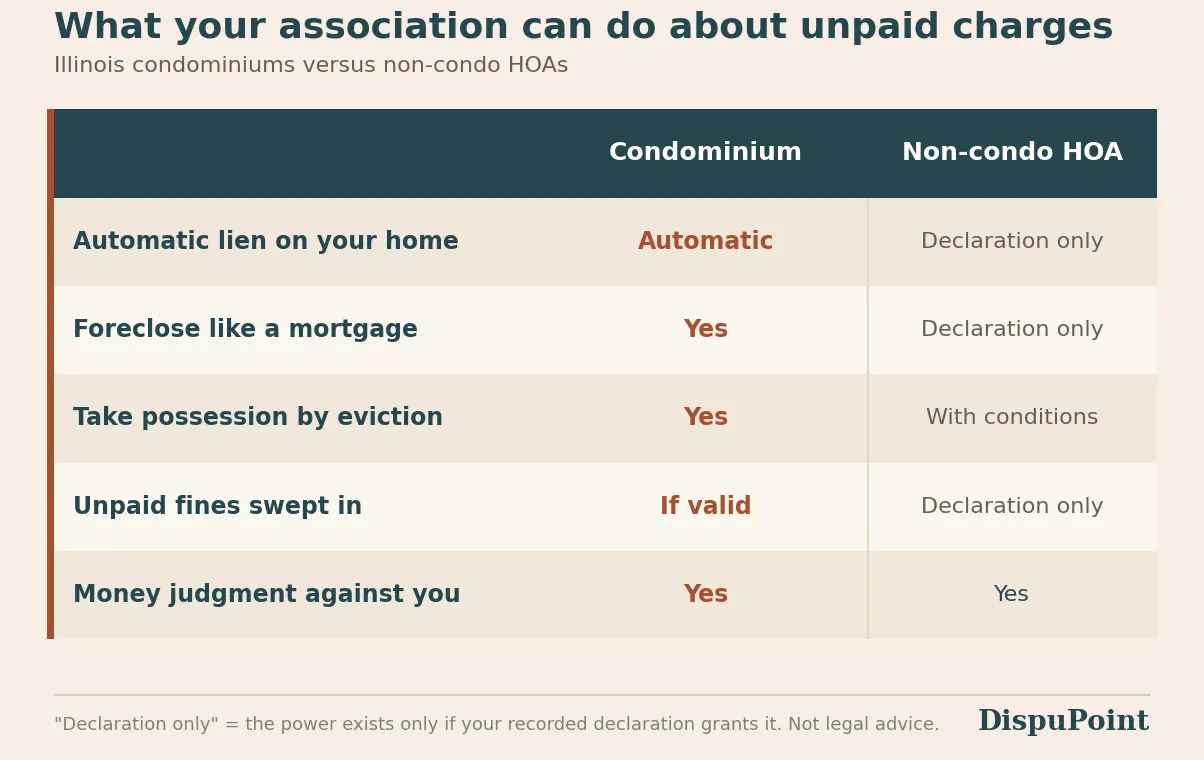

If you're in a condominium: the lien is automatic

Here the board has real teeth. Under the Condominium Property Act, a condo association gets an automatic lien the moment you fall behind, and it covers unpaid assessments, fines, interest, late charges, and collection costs. The association can foreclose that lien in court the same way a mortgage lender would, and it sits ahead of almost everything except property taxes and any mortgage recorded before it.

This is where paying off your mortgage cuts against you. With a loan on the property, the bank's claim usually sits ahead of the association's, so foreclosing rarely nets them much and they often don't bother. Pay the mortgage off, and that senior claim is gone. Now your equity is sitting right there in the open, which makes foreclosure a more realistic move for them, not less.

If you're in a non-condo HOA: there is no automatic lien

Now the part almost nobody knows. CICAA, the law covering non-condo HOAs, does not hand your association a lien. None. If your HOA wants to record a lien and foreclose, that power has to be written into your declaration. If the declaration doesn't grant it, the HOA simply doesn't have it, and the threat to take your house is mostly noise. So the first move is to read the declaration and find out whether the power even exists.

The route people don't see coming: eviction

Even without foreclosure, a non-condo HOA has another tool. Illinois' Eviction Act lets an association bring a possession action over unpaid assessments, usually after a 30-day written demand, as long as it meets the law's conditions. Win that, and the association takes possession and can rent your place out to cover the debt. You keep the title; you lose the keys. It isn't foreclosure, and the conditions the association has to satisfy are one more place these cases fall apart.

Fines are the shakiest foundation of all

Whatever bucket you land in, a fine has to be valid before it can anchor anything. Both the condo law and CICAA require your association to give you written notice of the alleged violation and a real chance to be heard before it imposes a fine. Skip that, and the fine is defective. A lien or a collection action built on a defective fine inherits the very same crack.

So ask, in writing, for two things: which specific rule did I break, and where was my hearing? Make the board point to the numbered provision in the governing documents and show the process it followed. A lot of boards go quiet right there, because the honest answer is that a step got skipped.

The gap that gets people in trouble

Here's the pattern I see over and over. Someone gets a notice, decides it's petty, tosses it, and stops opening mail from the board. Three months later there's a second notice with late fees. Six months on there's a lien, if the association even has that power. A year out there's a lawsuit. The charge was never the real problem. The silence after it was.

The board is counting on that silence. Every month you don't answer, the balance grows and the paper trail tilts their way. Respond in writing, dispute what's wrong, and pay the part that's genuinely owed while the contested part stays contested. That one move separates the issues and keeps you out of the collection lane. If you're weighing whether to just stop paying, we walk through why that usually backfires here.

How to respond in writing

A written response does three things at once. It creates a record, it puts the board on the clock, and it forces them to show their authority for every charge. If the board keeps stonewalling after that, there are ways to hold it accountable beyond a single letter, which we cover here. Send the letter certified, keep a copy, and ask for specifics.

How to

Dispute an HOA fine or lien notice in writing

Send this to your association or its management company by certified mail so you have proof it arrived, and keep a copy with your mailing receipt. This starts the paper trail and forces a written answer before anything escalates.

[Your Name] [Property Address] [Date] [Association Name] [Association or Management Company Address] Re: Dispute of Notice Dated [Date of Notice] - Lot/Unit [Number] Dear Board Members: I am writing to dispute the charge described in your notice dated [Date], in the amount of $[Amount], related to [brief description]. I am requesting the following in writing within 14 days: 1. The specific provision of the declaration, bylaws, or rules that authorizes this charge, and, if the notice concerns a fine, the specific rule I am alleged to have violated. 2. Written confirmation of the notice I received and the hearing I was offered before any fine was imposed. 3. The provision of the declaration, if any, that grants the association the right to record a lien or pursue foreclosure. 4. An itemized statement of my account showing how the balance was calculated. Until these items are provided, I consider this charge disputed and not validly assessed. I am prepared to attend a properly scheduled hearing. Please contact me at [Phone or Email]. Sincerely, [Your Name]

This letter puts the burden back on the board to prove its authority, and item three quietly tests whether the association even has foreclosure power to begin with. Boards that skipped a step, or never held the power they implied, tend to soften once the record is clear.

That letter is step one.

You can send the above letter, or we can handle the whole case ourselves, from start to finish.

Get my free assessmentNo payment now. The $249 only starts your case if you act.

FAQ

Can an HOA foreclose on a paid-off home in Illinois?

It depends on your community. A condominium association has an automatic lien under state law and can foreclose it in court, and a paid-off home actually raises your exposure because no mortgage sits ahead of the association. A non-condo HOA can only foreclose if its declaration grants that power in writing.

My HOA is threatening foreclosure. How do I know if it can actually do it?

Read your recorded declaration. For a non-condo HOA, foreclosure power isn't automatic; it exists only if the declaration spells it out. If those words aren't there, the association is likely limited to an eviction action or a money judgment, not taking your home. Get the document and check before you react to the threat.

What's the difference between an HOA lien and an HOA eviction in Illinois?

A lien is a claim recorded against your property that can, where authorized, be foreclosed to force a sale. An eviction action seeks possession instead: the association takes over the unit and can rent it out to cover the debt while you keep title. Non-condo HOAs often lean on eviction because CICAA gives them no automatic lien.

Can an Illinois HOA take my home over a single unpaid fine?

Rarely, and never easily. A fine has to be validly imposed first, with written notice and a hearing, or it's defective. For a non-condo HOA, a fine also can't reach foreclosure unless the declaration allows it. Boards seldom foreclose over a small fine because the cost dwarfs the amount, but balances grow fast when you go silent.

How much notice does an Illinois HOA have to give before it acts?

Before imposing a fine, the association owes you notice of the violation and a chance to be heard. Before an eviction action for unpaid assessments, associations generally send a written demand giving you a set time to pay, often 30 days. The exact timing lives in your governing documents, so read them next to whatever notice you received.

How do I dispute an HOA fine or lien notice in Illinois?

Send this to your association or its management company by certified mail so you have proof it arrived, and keep a copy with your mailing receipt. This starts the paper trail and forces a written answer before anything escalates.