The dues went up again. Or the board hit you with a fine for something that is not even in the rules, and now you are staring at the bill thinking the obvious thought: what if I just do not pay it?

Hold on. Read this first. The instinct to withhold is the exact one that gets Illinois homeowners hurt, and there is a better move that costs you less and leaves you standing on firmer ground.

What Illinois Law Actually Gives Your HOA

The hard part first. Whether you are in a condo association or an HOA, Illinois law hands your board a serious collection toolkit. Condos operate under the Illinois Condominium Property Act (765 ILCS 605). HOAs fall under the Common Interest Community Association Act, usually called CICAA (765 ILCS 160).

For a condo, that toolkit includes an automatic lien on your home the moment assessments go unpaid. For a non-condo HOA it works a little differently. The CICAA statute gives no automatic lien of its own, so whatever lien power your board has comes from your community's declaration instead. Either way, the first thing you should do is find out exactly what your own documents allow.

And a condo lien is not a warning letter. It attaches to your title.

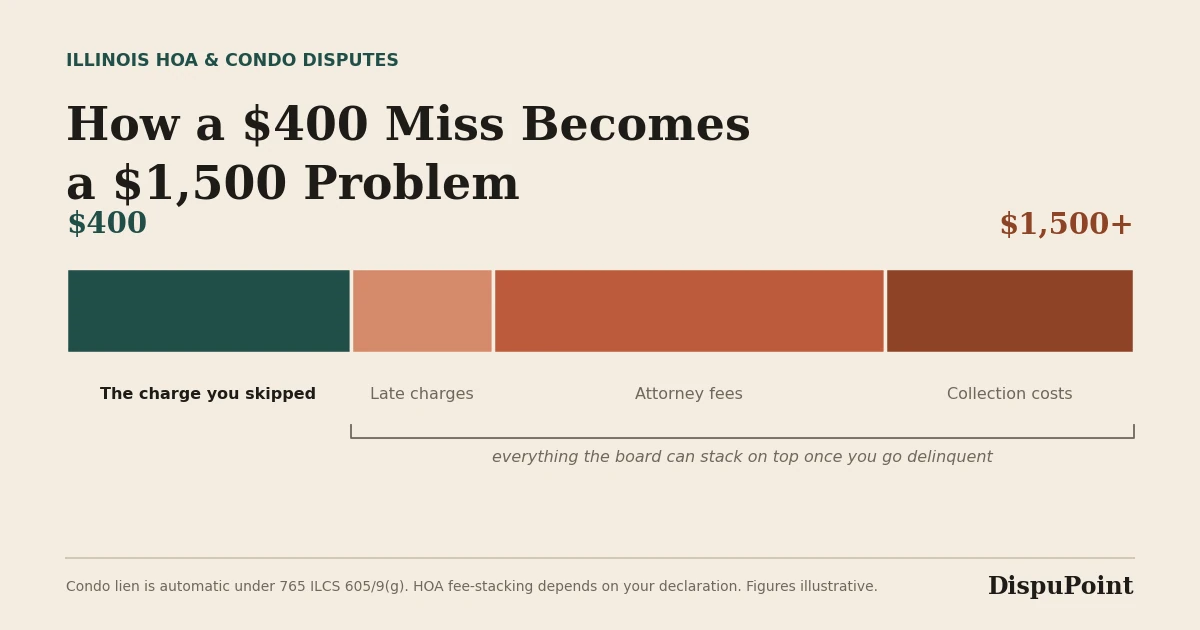

The Lien Comes First, Then It Gets Worse

Once that lien is recorded, it can wreck your ability to refinance or sell. A title company finds it. A buyer's lender objects to it. And it does not just follow you around, it follows the property itself.

Under 765 ILCS 605/9 for condos, the association can pile attorney fees, late charges, and collection costs on top of what you originally owed. For HOAs those same charges usually flow from your declaration rather than the statute, but they land in the same place. A $400 missed assessment turns into a $1,500 problem faster than you would believe.

Can Your HOA Actually Foreclose?

Yes. This is the part that shocks people. Illinois associations can foreclose over unpaid assessments, and the bar is lower than you would guess. A condo lien can be foreclosed the same way a mortgage is, and courts have backed it again and again.

A condo association can foreclose even when you are perfectly current on your mortgage. The two debts have nothing to do with each other. If that sounds alarming, good. It should.

So Do Your Homework First

Now the better move. Before you withhold a single dollar, find out whether you actually have a way out of this charge. That means the boring work: pull your bylaws, pull your declaration, and read the exact process the board was supposed to follow.

Was the fine issued without the notice your rules require? Was the special assessment voted on at a meeting nobody properly announced? Did the board skip a step it does not get to skip? This is where the real leverage lives, in the gap between what the board did and what its own documents say it had to do.

Be diligent. Be thorough. But do not let yourself slide into delinquency while you dig. The second you stop paying, you hand the board the exact weapon this whole article is about.

Pay Under Protest, Then Go After Them

Here is the play that actually works. If you cannot get the charge reversed up front, pay it, but pay it under protest, in writing, on the record. Then pursue the association to get it back.

Paying under protest keeps you current, and staying current strips the board of the lien, the stacked fees, and the foreclosure threat. It does not mean you agree with the charge. It does not mean you are finished. It means you took their best weapon off the table before the fight even started.

Now compare that to the alternative. You refuse to pay. The board records a lien, the fees stack, the collection costs climb, and suddenly you are fighting from underneath a recorded debt instead of from level ground. Chasing a wrong charge you already paid is cheaper and far more effective than defending one you let harden into a lien.

One honest caveat. Writing "under protest" on a check is not a magic spell, and it does not by itself get your money back. What it does is keep you out of the hole and build a clean record that you disputed the charge from day one. That record is what carries weight later, whether it lands in front of a board hearing or a small claims judge.

Put the Dispute in Writing

Whatever you decide about payment, the dispute itself has to be in writing. A phone call to the property manager evaporates. A certified letter does not.

How to

Dispute an improper HOA fee or fine in writing

Send this letter to your HOA or condo board by certified mail, return receipt requested, before your next due date. It preserves your rights and starts the formal record.

[Date] [Your Name] [Your Address] [City, IL ZIP] [HOA/Condo Association Name] Board of Directors [Association Mailing Address] Re: Formal Dispute of Assessment/Fine - Account [Your Unit or Lot Number] Dear Board of Directors, I am writing to formally dispute the [fee/fine/special assessment] of $[amount] dated [date], which appears on my account. My grounds for dispute are as follows: 1. [Describe the specific charge - for example: "This fine was issued without prior written notice of violation as required by the association's rules."] 2. [Describe any procedural issue - for example: "The special assessment was not approved at a properly noticed meeting open to all members."] 3. [Describe any factual disagreement - for example: "The violation described did not occur, as documented by the attached photographs dated [date]."] I request that the board review this charge at its next meeting and provide a written response within 30 days. I am prepared to attend a hearing if the association's rules provide for one. I am paying this charge under protest and reserve all rights under the Illinois [Condominium Property Act, 765 ILCS 605 / Common Interest Community Association Act, 765 ILCS 160]. Sincerely, [Your Name] [Phone / Email]

A written dispute sent by certified mail creates a timestamped record the board has to address, and it puts your objection on file before any lien is ever recorded.

What If the Board Just Ignores You?

Boards do ignore written disputes sometimes. If yours does, your next step is escalating inside the process your governing documents lay out, which usually means a hearing in front of the board. Under CICAA, an HOA that levies fines has to give a member notice and a chance to be heard first. Jumping straight to a lawsuit and skipping that step is almost always slower and more expensive.

Document everything. Their responses, their silences, the meeting minutes, every payment you make. That file is your single best asset if this ever reaches a judge.

The One Thing You Should Not Do

Do not go quiet. Homeowners who stop paying and stop answering end up with recorded liens, collection agencies, and sometimes a foreclosure suit, and every one of those costs far more to undo than the original dispute would have cost to fight.

If the charge is wrong, say so in writing, pay under protest, and keep saying so. If you genuinely cannot pay, tell the board that in writing and ask about a payment plan. Associations would rather collect your money than run a foreclosure.

---

FAQ

How do I formally dispute an HOA fine in Illinois?

Send a written letter to the board by certified mail before your next due date. Name the charge, state your grounds, and cite the relevant statute, 765 ILCS 605 for condos or 765 ILCS 160 for HOAs. Ask for a written response and a hearing, and keep a copy of everything.

Can my HOA put a lien on my house for unpaid dues?

For a condo, yes, automatically under the Illinois Condominium Property Act the moment assessments go unpaid. For a non-condo HOA, only if the association's declaration grants that right, since CICAA creates no automatic lien. A condo lien can include attorney fees and collection costs and shows up on any title search.

Can an HOA foreclose on my home in Illinois?

Yes. Illinois courts allow condo and HOA foreclosure actions for unpaid assessments, and a condo lien can be foreclosed the same way a mortgage is. Being current on your mortgage does not protect you from an association foreclosure.

Should I pay a charge I think is wrong, or withhold it?

Pay it, under protest and in writing, then pursue the association to get it back. Paying keeps you current and strips the board of its lien and foreclosure leverage. Withholding does the opposite and usually leaves you fighting from a weaker position.

Will withholding dues force my HOA to negotiate with me?

Rarely, and it usually backfires. Associations have strong legal tools and tend to accelerate collection once payments stop, not soften. Paying under protest while you dispute the charge in writing almost always leaves you better off than going delinquent.